Wide Variation in Hospital and Physician Payment Rates Evidence of Provider Market Power

HSC Research Brief No. 16

November 2010

Paul B. Ginsburg

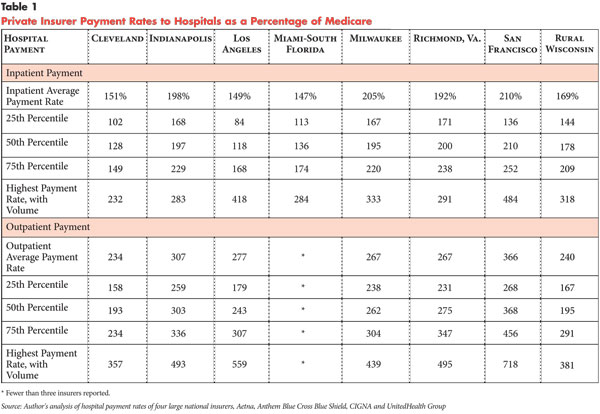

Wide variation in private insurer payment rates to hospitals and physicians across and within local markets suggests that some providers, particularly hospitals, have significant market power to negotiate higher-than-competitive prices, according to a new study by the Center for Studying Health System Change (HSC). Looking across eight health care markets—Cleveland; Indianapolis; Los Angeles; Miami; Milwaukee; Richmond, Va.; San Francisco; and rural Wisconsin—average inpatient hospital payment rates of four large national insurers ranged from 147 percent of Medicare in Miami to 210 percent in San Francisco. In extreme cases, some hospitals command almost five times what Medicare pays for inpatient services and more than seven times what Medicare pays for outpatient care. Variation within markets was just as dramatic. For example, the hospital with prices at the 25th percentile of Los Angeles hospitals received 84 percent of Medicare rates for inpatient care, while the hospital with prices at the 75th percentile received 184 percent of Medicare rates. The highest-priced Los Angeles hospital with substantial inpatient claims volume received 418 percent of Medicare. While not as pronounced, significant variation in physician payment rates also exists across and within markets and by specialty. Few would characterize the variation in hospital and physician payment rates found in this study to be consistent with a highly competitive market. Purchasers and public policy makers can address provider market power, or the ability to negotiate higher-than-competitive prices, through two distinct approaches. One is to pursue market approaches to strengthen competitive forces, while the other is to constrain payment rates through regulation.

- Many Providers Have Upper Hand in Payment Negotiations

- Inpatient Hospital Payment Variation Across Markets

- Payment Variation Within Markets More Striking

- Outpatient Hospital Payment Rates

- Physician Payment

- Policy Implications

- A Market Approach

- A Regulatory Approach

- Notes

- Data Source and Funding Acknowledgement

Many Providers Have Upper Hand in Payment Negotiations

![]() s health care affordability issues intensify, the issue of provider market power over private insurers, or their ability to negotiate higher-than-competitive payment rates, is moving squarely onto the policy radar screen.1 Under national health reform, coverage expansions and Medicare and Medicaid payment reductions to hospitals may lead to even higher private insurer payment rates.

s health care affordability issues intensify, the issue of provider market power over private insurers, or their ability to negotiate higher-than-competitive payment rates, is moving squarely onto the policy radar screen.1 Under national health reform, coverage expansions and Medicare and Medicaid payment reductions to hospitals may lead to even higher private insurer payment rates.

During HSC’s recently completed 2010 site visits to 12 nationally representative metropolitan communities, insurers consistently cited higher payment rates to obtain hospital and physician group participation in health plan networks as a major factor driving higher insurance premiums.2 Hospitals often acknowledged that private insurance rates were rising more rapidly than their costs but attributed the spread to increasingly constrained Medicare and Medicaid payment rates.

The Medicare Payment Advisory Commission (MedPAC) has found that hospitals with substantial negotiating leverage can allow unit costs to rise because they can obtain higher private insurance rates to offset negative Medicare margins that result from their high costs.3 Previous HSC research examining six California metropolitan areas documented considerable increases in provider leverage over time, resulting in striking differences in payment rates to providers with strong leverage vs. those with little leverage.4 With the enactment of the Patient Protection and Affordable Care Act (PPACA), some fear that the opportunity for hospitals, physicians and other providers to form so-called accountable care organizations (ACOs) to contract with Medicare will further increase their leverage over private health plans.

This study analyzed data on private insurer payment rates to hospitals and physician practices, focusing on variation across and within markets. Four major insurers provided payment rate data in eight market areas, reporting their private payment rates as percentages of Medicare payment rates (see Data Source). The results show large differences in payment rates across the eight markets and even larger differences within individual markets. To gain additional insights, interviews were conducted with representatives of the four insurers and provider trade and professional associations.

Back to Top

Inpatient Hospital Payment Variation Across Markets

![]() verage inpatient payment rates in the eight market areas varied widely, ranging from 147 percent of Medicare rates in Miami to 210 percent in San Francisco (see Table 1). Indianapolis, Milwaukee, rural Wisconsin and Richmond stood out as high-priced markets for private insurers relative to Medicare. More moderate markets included Cleveland and Los Angeles.

verage inpatient payment rates in the eight market areas varied widely, ranging from 147 percent of Medicare rates in Miami to 210 percent in San Francisco (see Table 1). Indianapolis, Milwaukee, rural Wisconsin and Richmond stood out as high-priced markets for private insurers relative to Medicare. More moderate markets included Cleveland and Los Angeles.

The payment-rate patterns reported by individual insurers showed broad similarities but important differences across the eight markets. For example, although San Francisco had the highest average rate across the four insurers, it was the highest-priced market for only two insurers. Presumably, this reflects such factors as health plans’ differing market shares in the eight communities.

Explaining the pattern of relative rates across markets is difficult because many factors likely play a role, including the overall degree of hospital concentration in particular markets. But some metropolitan areas have hospital markets smaller than the metropolitan area, so that without a high overall degree of concentration in the metropolitan areas, single hospital systems dominate markets within them. Hospital reputation also plays an important role. In some markets, certain hospitals are so highly regarded that consumers perceive any health plan network that excludes these “must-have” hospitals as undesirable. Some markets have such marquee hospitals, but others do not.

Within a hospital system, a highly regarded flagship hospital can lead to higher rates for the system’s more ordinary hospitals, since hospital systems often have the clout to negotiate rates as a single entity. Those who believe that cost shifting is important point to relatively low Medicaid payment rates in some areas leading to higher payment rates for private insurers. In economic parlance, cost shifting means that health care providers do not fully exercise their market power to maximize profits so that they are in a position to raise rates to private payers in response to cuts in public payer rates.

Looking at the eight communities, informed conjecture is possible about why hospitals in some communities can command higher rates. San Francisco has a high degree of hospital concentration and must-have hospitals, coupled with low Medicaid rates. Richmond, like many smaller metropolitan areas, has a highly concentrated hospital market—two systems and an academic medical center. Milwaukee’s high rates, which have been documented elsewhere,6 probably result from a combination of hospital concentration and dominance in submarkets.

Likewise, Indianapolis is not highly concentrated overall but has a number of distinct markets within the metropolitan area where a particular hospital system dominates. Rural Wisconsin, like most rural areas, is comprised of hospitals with no competitors in their communities and heavy dependence on Medicare and Medicaid patients. Cleveland has a highly concentrated hospital market but has notably lower rates than other highly concentrated markets. A history of a major insurer excluding the downtown hospitals of one of the market’s two major systems from the plan’s network and the broad geographic coverage of each of the systems may diminish the systems’ ability to raise rates. Los Angeles has a relatively fragmented hospital market with many small hospitals that lack must-have status for inclusion in insurer provider networks but also a small number of marquee hospitals. Miami has a relatively low degree of concentration, although some hospital systems are perceived as powerful in submarkets.

The average inpatient rates overall appear to be generally consistent with MedPAC data, although the eight markets are not nationally representative. Calculations from the most current published MedPAC data suggest that private insurer payment rates averaged 139 percent of Medicare rates nationally in 2008.7

Back to Top

Payment Variation Within Markets More Striking

![]() ariation within each market was even more striking than variation across the eight markets. Insurers were asked to arrange hospital payment rates—the unit is the hospital—within markets in ascending order and report by quartile. Rates at the 50th percentile (median) show a pattern generally similar to the individual market averages, but distinct results emerge at other points in the distribution.

ariation within each market was even more striking than variation across the eight markets. Insurers were asked to arrange hospital payment rates—the unit is the hospital—within markets in ascending order and report by quartile. Rates at the 50th percentile (median) show a pattern generally similar to the individual market averages, but distinct results emerge at other points in the distribution.

In Los Angeles, the rate at the 25th percentile of hospitals was 84 percent of Medicare rates, while the highest payment rate to a single Los Angeles hospital was 418 percent of Medicare. Moreover, all four insurers reported a very high rate for their top hospital in Los Angeles—possibly the same hospital. Previous research has indicated stark contrasts in payment rates commanded by Los Angeles’ so-called have and have-not hospitals.8 While Cedars Sinai and UCLA have strong reputations, many Los Angeles hospitals are indistinct from others a few miles away.

Within communities, hospitals with higher payment rates tended to be the larger hospitals. For example, a disproportionate share of spending occurred at hospitals at or above the 75th percentile (findings not shown)—an expected finding since larger hospitals are likely to have more leverage with health plans.

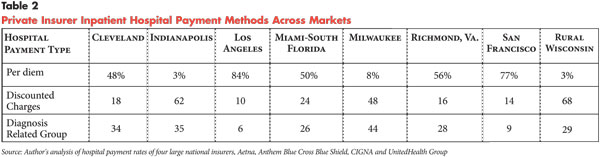

Insurers pay hospitals for inpatient care by three distinct methods—diagnosis related groups (DRGs), per diems or discounted charges. Variation by market in payment methods is large (see Table 2). For example, DRGs, or other case rate payment, ranged from 47 percent in Indianapolis to 6 percent in Los Angeles. Responses from individual insurers indicated that within some markets, different insurers used different payment methods. In interviews, insurers asserted a preference for DRGs over other payment methods because broader payment units provide more control over total payments.

One would think that hospitals would prefer DRGs as well—in addition to Medicare, almost all Medicaid programs use DRGs—because consistent methods across payers would align the incentives hospitals face from different payers. Whether through inertia or resistance, distinct norms have been established in different parts of the country. Aside from insurers with larger market shares having more standing to engage hospitals in discussions about which payment methods to use, there was little indication that payment methods were determined by the relative market power of hospitals and insurers. After all, it would be much more straightforward for a hospital simply to seek higher rates rather than to negotiate a change in the payment mechanism. To the degree that a particular payment method, such as DRGs, is seen as advantageous from a societal perspective, policy makers should not assume that the market forces present today will bring it about.

Outpatient Hospital Payment Rate

![]() ayment rates for hospital outpatient services were generally higher—in relation to Medicare rates—than those for inpatient services. This is somewhat unexpected, since hospitals face some degree of competition for outpatient services from freestanding facilities, such as ambulatory surgical centers, imaging centers and physician offices. Medicare hospital outpatient margins were lower than inpatient margins in 2008 by roughly 8 percentage points, -12.9 percent vs. -4.7 percent.9 However, the degree to which private insurer outpatient payment rates in relation to Medicare in the eight communities are higher than inpatient rates exceeded the difference in Medicare margins. Since all of a hospital’s services typically are covered in a network agreement, whether a hospital’s inpatient or outpatient services have greater must-have status to consumers is unlikely to lead to such large rate differences relative to Medicare.

ayment rates for hospital outpatient services were generally higher—in relation to Medicare rates—than those for inpatient services. This is somewhat unexpected, since hospitals face some degree of competition for outpatient services from freestanding facilities, such as ambulatory surgical centers, imaging centers and physician offices. Medicare hospital outpatient margins were lower than inpatient margins in 2008 by roughly 8 percentage points, -12.9 percent vs. -4.7 percent.9 However, the degree to which private insurer outpatient payment rates in relation to Medicare in the eight communities are higher than inpatient rates exceeded the difference in Medicare margins. Since all of a hospital’s services typically are covered in a network agreement, whether a hospital’s inpatient or outpatient services have greater must-have status to consumers is unlikely to lead to such large rate differences relative to Medicare.

The pattern of substantially higher private rates for outpatient care could be an artifact from the era when Medicare inpatient care was paid prospectively through DRGs while outpatient payment was cost based. Hospitals had an incentive to load overhead onto outpatient services—which is no longer the case—and this legacy may influence pricing for private insurers. In other words, a different allocation of overhead between inpatient and outpatient services could lead to what would appear to be a more uniform difference from Medicare rates.

Whatever the basis, the pattern of higher rates for outpatient care in relation to Medicare rates implies that hospitals perceive limited price competition from freestanding facilities. This may reflect the fact that, except for high-deductible health plans, most insurance benefit designs do not reward patients financially for choosing freestanding outpatient facilities over hospital outpatient departments. Or, it could reflect the rapidly increasing alignment between hospitals and physicians, which might give hospitals more confidence that patients will be referred to their outpatient facilities. Another possibility is growing hospital ownership of freestanding facilities through joint ventures with physicians. And, in some states, hospitals have been able to use the certificate-of-need process to block entry by physician-owned facilities.

The pattern of variation of hospital outpatient payment rates across and within markets is similar to the pattern for inpatient services. Since inpatient and outpatient rates are covered in a single negotiation between a hospital and an insurer, this is not surprising. Discussions with insurers about payment methods for hospital outpatient services indicated the same desire—as with inpatient care—to use broader payment units. Interviews suggested that use of the Medicare ambulatory payment classification (APC) system as a basis for private insurance payment is growing but still not widespread. Insurers identified discounted charges as the most common payment method for hospital outpatient services.

Back to Top

Physician Payment

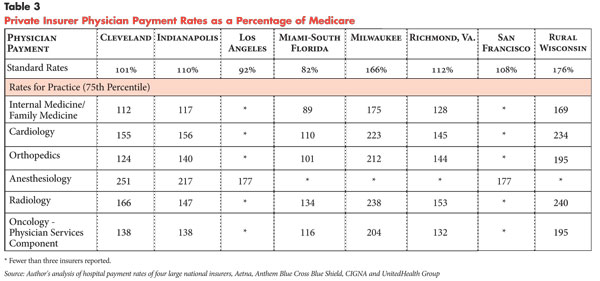

![]() hysician payment rates are easier to communicate because of the almost universal use by private insurers of the Medicare physician fee schedule. Most insurers create fee schedules based on the Medicare fee schedule relative value scale but use their own conversion factors, which reflect the intersection of their goals for the number of physicians participating in each network and local physician supply. For most small physician practices, insurers quote their fee schedule, and the practice either accepts the schedule and participates in the network or does not participate and instead bills patients as an out-of-network provider. Larger practices negotiate higher rates with insurers based on the perceived importance of their presence in plans’ networks. Standard—not negotiated—rates tend to be based on a common fee schedule for most specialties, but there are important exceptions, such as hospital-based specialties, particularly anesthesiology.

hysician payment rates are easier to communicate because of the almost universal use by private insurers of the Medicare physician fee schedule. Most insurers create fee schedules based on the Medicare fee schedule relative value scale but use their own conversion factors, which reflect the intersection of their goals for the number of physicians participating in each network and local physician supply. For most small physician practices, insurers quote their fee schedule, and the practice either accepts the schedule and participates in the network or does not participate and instead bills patients as an out-of-network provider. Larger practices negotiate higher rates with insurers based on the perceived importance of their presence in plans’ networks. Standard—not negotiated—rates tend to be based on a common fee schedule for most specialties, but there are important exceptions, such as hospital-based specialties, particularly anesthesiology.

Average standard physician rates across the eight markets were within 20 percent of Medicare rates in most of the geographic areas (see Table 3). Miami had the lowest rates, while Milwaukee and rural Wisconsin stood out at the high end.

Standard rates tend not to apply to hospital-based specialists. Although reporting of rates for anesthesiologists for this study was limited, rates were substantially higher than for other specialties. Radiologists also received higher rates but not as high as anesthesiologists.

Insurance executives explained the high rates for anesthesiologists are a consequence of patients’ inability to choose an anesthesiologist. Since hospitals tend to contract with one or more anesthesiology groups to provide all services, insurers perceive that it would be inappropriate to penalize enrollees using an in-network hospital for using an out-of-network anesthesiologist. This leads to insurers seeking to obtain a much higher percentage of anesthesiologists in their networks than for other specialties. In the parlance of the earlier hospital rate discussion, most anesthesiology groups are must-have providers for insurance networks, although in this case the status comes not from reputation but patients’ inability to choose.

It is noteworthy that insurers apparently cannot make anesthesiologist participation in an insurer’s network a requirement for hospital participation in the network, and that hospitals apparently cannot require anesthesiologists to participate in the same networks as the hospital as a condition of receiving hospital privileges.

While negotiated payment rates at the 75th percentile for certain physician specialties in each community were substantially higher than the standard rates, they were generally not as high—in relation to Medicare—as hospital rates. Community rankings varied by specialty, likely because of such local market factors as the degree to which specialty physicians practice in large groups. At the 75th percentile, rates for primary care physicians tended to be substantially lower than for other specialties, likely reflecting stronger negotiating leverage of single-specialty groups.

Formation of larger groups has been far more prevalent for specialists than for primary care physicians. So insurers can follow the Medicare fee schedule and not vary standard rates by specialty, but at the end of the negotiating process, many specialists are paid substantially more than primary care physicians.10

Similar to hospital rates, physician rates in Milwaukee and rural Wisconsin were generally higher than in other communities. A likely factor behind high rates in Milwaukee is that most physicians are employed by hospitals, and their rates are negotiated by the hospitals. This allows hospitals to broaden their leverage for inpatient and outpatient facility services to professional payment for physician services. Rates in rural Wisconsin may be high because insurers need a higher proportion of physicians included in their networks in rural areas than is the case in urban areas.

Rates at the 75th percentile for most specialties in Los Angeles and San Francisco could not be included in the table because too few insurers reported them, but both had relatively high rates. Both communities have large, highly regarded medical groups considered essential for inclusion in insurers’ networks. And, California has extensive regulation of health maintenance organization (HMO) networks requiring adequate access to physicians, which may also give physicians some degree of leverage.

Policy Implications

![]() ew would characterize the variation in hospital and physician payment rates found in this study to be consistent with what would be expected in a highly competitive market—at least for markets outside of health care. Indeed, observers of markets outside of health care would be stunned by the degree of price variation. A highly competitive market would have variation in payment rates across communities and across providers within a community that reflect the cost differences outside of the control of providers, such as differences in labor costs in different locales, and differences in quality. Medicare payment methods are designed to capture cost differences outside of the control of providers through case-mix adjustments, medical education adjustments and input-price indexes. Since payment rates are expressed as a percentage of Medicare rates, these factors, in theory, have been taken into account.

ew would characterize the variation in hospital and physician payment rates found in this study to be consistent with what would be expected in a highly competitive market—at least for markets outside of health care. Indeed, observers of markets outside of health care would be stunned by the degree of price variation. A highly competitive market would have variation in payment rates across communities and across providers within a community that reflect the cost differences outside of the control of providers, such as differences in labor costs in different locales, and differences in quality. Medicare payment methods are designed to capture cost differences outside of the control of providers through case-mix adjustments, medical education adjustments and input-price indexes. Since payment rates are expressed as a percentage of Medicare rates, these factors, in theory, have been taken into account.

In a competitive market, much of the price differences associated with quality differences would reflect costs associated with producing higher quality. Although measurement of health care quality remains rudimentary, it is unlikely costs associated with differences in quality across the eight areas studied would be as large as the differences in payment rates. Differences in patient severity not picked up by Medicare adjustments could be a factor but are likely to be more relevant to differences in rates across individual providers than across areas. Some of the payment rate variation might be explained by other factors, such as Medicaid rates being much lower in some states than in others or differences in hospitals’ uncompensated care burdens. But the degree of differences suggests that variation in market power is important.

A number of factors likely contribute to competition being weak. There has been extensive provider consolidation over time, initially by creation of hospital systems through mergers and acquisitions, and more recently through mergers of group medical practices and increasing hospital employment of physicians. The nature of insurance benefit structures plays a role as well. A lasting legacy of the move toward managed care in the 1980s and ‘90s is that privately insured people still typically pay only a small proportion of the costs of their care out of pocket. Though patient cost sharing has increased steadily since the early part of the decade, benefit designs have not focused on encouraging patients to choose lower-cost providers. Indeed, a remaining influence of the managed care backlash is that insurers continue to be pressed by purchasers to maintain networks that allow a broad choice of providers, contributing to the must-have status of some providers. The lack of meaningful information on provider quality also makes consumers reluctant to choose providers based on price for services other than those that are simple and standardized.

The price variation identified across the eight areas suggests that provider market power is more of a problem in some markets than others. And, price variation within a market indicates some providers have much more leverage than others. Purchasers and policy makers can address weak competitive forces through two distinct approaches. One is to pursue market approaches to strengthen competitive forces, while the other is to constrain prices through regulation.

Back to Top

A Market Approach

![]() he essence of the market approach is redesigning insurance benefit structures so that more patients have strong incentives to choose providers with lower overall costs. Ability to do this effectively has been increasing, with tools such as episode groupers that allow insurers to make more accurate assessments of the relative costliness of different providers. Instead of being limited to comparing hospital room charges or payment for a day in the hospital, episode groupers permit comparison of the total payment for all services across all care settings involved in an episode of care. Groupers also permit calculation of some quality elements that are highly related to costs, such as rates of potentially avoidable complications. Although physicians have criticized the proprietary episode groupers now used because they lack transparency, the PPACA requires the Centers for Medicare and Medicaid Services to develop a public domain episode grouper with provider input.

he essence of the market approach is redesigning insurance benefit structures so that more patients have strong incentives to choose providers with lower overall costs. Ability to do this effectively has been increasing, with tools such as episode groupers that allow insurers to make more accurate assessments of the relative costliness of different providers. Instead of being limited to comparing hospital room charges or payment for a day in the hospital, episode groupers permit comparison of the total payment for all services across all care settings involved in an episode of care. Groupers also permit calculation of some quality elements that are highly related to costs, such as rates of potentially avoidable complications. Although physicians have criticized the proprietary episode groupers now used because they lack transparency, the PPACA requires the Centers for Medicare and Medicaid Services to develop a public domain episode grouper with provider input.

Better data on the quality of care for patients also would enhance the effectiveness of incentives to encourage them to consider price when choosing providers. For the most part, such data are not yet widely available, although methods for measuring and public reporting of quality data are improving.

Benefit designs that encourage patients to compare providers on the basis of price are not common today but are developing. Narrow-network insurance products, which exclude selected high-cost providers from a network, are attracting some interest, especially among small employers. Still stung by the backlash against tightly managed care in the mid-1990s, many employers have resisted efforts to limit provider networks, instead relying on increased patient cost sharing to slow premium growth. But relentless affordability pressures are leading some employers to rethink that strategy and consider narrow-network plans.

Another benefit design, known as tiered networks, emphasizes consumer incentives to choose lower-cost providers. Consumers are familiar with the concept because of its extensive use in prescription drug benefits, where they typically pay the least for generic drugs, a larger amount for preferred brand-name drugs and the most for non-preferred brand-name drugs. When this approach is applied to hospital and physician services, aspects of patient cost sharing, such as the deductible, the coinsurance rate or copayments vary with the tier of the provider. More sophisticated versions of this approach would place hospitals—or even physicians—into tiers by category of services. Similar to narrow-network products, improved measurement of cost and quality would increase the effectiveness of tiered networks and, perhaps, lead to greater consumer and provider acceptance.

A critical factor holding back the spread of benefit designs that provide incentives for consumers to choose less expensive providers is the tax treatment of employer-sponsored health insurance. The fact that employer contributions and most employee contributions to health insurance come from pre-tax earnings dilutes the motivation to obtain health insurance with lower premiums. Under PPACA, however, starting in 2018, employer and pre-tax employee contributions exceeding $10,200 for single coverage or $27,500 for family coverage will be subject to a 40 percent excise tax. Since the threshold will not increase as quickly as premiums are likely to, over time an increasing percentage of people will have employer coverage subject to the tax and become more sensitive to the level of health insurance premiums.

Other policy changes that would support a market approach are in the antitrust arena. Following a wave of hospital mergers in the 1990s, hospital markets in many communities are highly concentrated. The Federal Trade Commission (FTC) attempted to block a number of mergers during the 1990s without success. Antitrust enforcement might be more successful going forward since research now offers stronger support that nonprofit hospital mergers increase prices.11 Nevertheless, it is difficult to conceive of any large-scale break up of hospital systems formed a decade or longer ago.

A new antitrust issue on the horizon concerns the formation of ACOs authorized by the health reform law. Under the law, Medicare can contract for care for a population of beneficiaries with “groups of providers of services and suppliers which have established a mechanism for shared governance.”12 Eligible groups include “ACO professionals in group practice arrangements, networks of individual practices of ACO professionals, partnerships or joint venture arrangements between hospitals and ACO professionals, hospitals employing ACO professionals, [and] such other groups of providers of services and suppliers as the Secretary determines appropriate.”13 The formation of Medicare ACOs could increase provider leverage in rate negotiations with private insurers, especially if ACOs lead to mergers between hospitals and medical groups or to hospitals increasing employment of physicians.

Currently, antitrust rules allow organizations that assume financial risk for patients’ care to negotiate private insurer payment rates on behalf of participating providers. Even provider groups that do not assume risk but can demonstrate a certain degree of clinical integration can negotiate as a group. Provider leverage could increase if the FTC—based on a presumption that all ACOs are clinically integrated—grants ACOs permission to negotiate with private insurers on behalf of all associated providers, even for contracts that do not involve risk. On the other hand, if the FTC does not grant such permission, the ACO would be unable to negotiate rates for non-risk contracts; each provider in the ACO would then have to negotiate individually with insurers. The ability to contract separately with providers would help maintain private insurers’ leverage with providers. The FTC may need to rethink policies allowing clinically integrated organizations to negotiate contracts that do not involve risk.

Two factors raise questions about whether market approaches could be sufficiently vigorous to lower payment rates substantially by reducing provider leverage. One is the degree to which a significant proportion of markets are so highly concentrated that effective competition is not possible. For example, many smaller communities, including some metropolitan areas, have only one hospital system. The trend of hospital employment of physicians further increases the market power of these hospitals.

The second is whether the public would support an approach that would force patients to consider price when choosing their physicians and hospitals. Most privately insured Americans are enrolled in preferred provider organizations (PPOs) with fairly comprehensive benefits and do not have to incorporate price into choosing a provider. Many political leaders have long resisted market approaches in health care—believing that market forces should not play a role in allocating health care, which should be done on the basis of medical need.

On the other hand, few political leaders have advocated higher patient cost sharing—such as large deductibles—to address the problem of rising health care costs. But, over the past decade, substantial increases in patient cost sharing in private insurance were used to slow rising premiums, with little apparent public backlash. Although PPACA limits the overall degree of patient cost sharing, what is permitted is far more extensive than the current norms in private insurance. With the increasing affordability pressures on employers and with the federal government soon to be subsidizing private coverage for those with incomes below 400 percent of poverty, political attitudes toward market approaches might change.

Back to Top

A Regulatory Approach

![]() regulatory approach to controlling provider market power would involve government placing ceilings on what providers can charge private insurers and individuals and establishing a common payment method across public and private payers. A number of states adopted this approach, known as all-payer rate setting, during the 1970s and 1980s to limit hospital rates. Most states abandoned their rate-setting programs in response to two developments. The first was a belief that Medicare inpatient prospective payment, enacted in 1983, would lead hospitals to contain costs and that additional regulation at the state level was not needed. The second was the expansion of tightly managed care and credible insurer threats to exclude providers from plan networks if provider payment rate demands were too high. A shift in the political climate toward deregulation also played a role.

regulatory approach to controlling provider market power would involve government placing ceilings on what providers can charge private insurers and individuals and establishing a common payment method across public and private payers. A number of states adopted this approach, known as all-payer rate setting, during the 1970s and 1980s to limit hospital rates. Most states abandoned their rate-setting programs in response to two developments. The first was a belief that Medicare inpatient prospective payment, enacted in 1983, would lead hospitals to contain costs and that additional regulation at the state level was not needed. The second was the expansion of tightly managed care and credible insurer threats to exclude providers from plan networks if provider payment rate demands were too high. A shift in the political climate toward deregulation also played a role.

Only Maryland and West Virginia have retained rate-setting systems. Maryland is broadening its system to include physician services delivered in hospitals. The Maryland system has generally had stronger hospital support than programs in other states, possibly because of a governance structure based on an independent commission insulated from political interference.14

Concerned about growing provider market power, some policy makers are reconsidering all-payer rate setting, especially at the state level. The landscape for rate setting is quite different now in three key ways than in the 1970s. First, differences in payment rates among private and public payers have become so large over time that equalizing payment rates across payers is unlikely to be feasible given the potential fiscal impact on Medicare and Medicaid—freezing differences is more plausible.

Second, there is the potential for these initiatives to pave the way for broader provider payment reform. For example, a Massachusetts commission charged with addressing how to contain costs has recommended that the state design a global payment system, an approach resembling ACOs in some respects, which all payers would use. A common payment method across payers would create consistent incentives for providers and likely accelerate the pace of provider payment reform. Although the proposal did not include regulation of the global rates, some Massachusetts providers expect this will ultimately occur.15 The third difference is the potential to incorporate physician payment as well as hospital payment.

However, specifying a method of provider payment, while an advantage in the short run as a mechanism to accelerate payment reform, has a downside of potentially locking in a system that turns out not be a good one. In contrast to the situation in the early 1980s, when Medicare adoption of DRG payment was seen as a clear improvement over the earlier cost-reimbursement or charge-based systems, consensus about how to reform provider payment is lacking. Although ACOs are encouraged under PPACA, the legislation also supports Medicare pilots of other methods, such as bundled payment, and requires the use of value-based purchasing by Medicare.

As with all regulatory approaches, there is concern that politics will play too large a role in the rate-setting process. This has been seen in certificate-of-need regulation, where politically powerful local hospital systems have often circumvented the process and where research suggests little has been accomplished in terms of cost containment.16

Given the lack of familiarity with the concept of all-payer rate setting today, a general political environment growing increasingly unreceptive to regulation and the fact that approaches to provider payment reform are just starting, this may not be a propitious time to pursue this option at the national level. However, some states, especially in the Northeast, with stronger preferences for regulatory approaches over market approaches, might decide to pursue rate setting now, seeking a Medicare waiver so that the approach would apply to all payers. Nationally, it might be more effective to devote the next few years to piloting different approaches to provider payment reform in the Medicare and Medicaid programs and in private insurance.

At the same time, efforts to use market approaches more effectively than has been done to date could be explored. Perhaps, the weak economy will push employers to more seriously consider benefit designs that limit provider choice or emphasize price when choosing a provider, much in the same way that the recession in the early 1990s pushed employers toward managed care. Government could support private-sector approaches by making Medicare provider data accessible to private insurers and rethinking antitrust policy. The latter would have to balance fostering needed clinical integration among providers and increasing provider market power that comes from greater alignment of providers.

Neither market nor regulatory approaches to constraining provider market power and constraining health care spending growth will be politically popular. Hard choices and trade-offs will be needed. But the failure to act to constrain spending growth will result in declining access to high-quality care for many Americans over the longer run and undermine the nation’s fiscal health.

Back to Top

Notes

Back to Top

Data Source

This Research Brief is based on data obtained from four national insurers—Aetna, Anthem Blue Cross Blue Shield, CIGNA and UnitedHealth Group—on current provider payment rates for eight geographic areas. The eight areas were purposively selected because it was believed they have a wide range of payment rates, with estimates based on a 2005 U.S. Government Accountability Office study of prices paid in the Federal Employees Health Benefits Program.5

All payment rates were reported as a percentage of Medicare rates, regardless of the payment unit actually used. For inpatient and outpatient hospital care, this meant that each insurer had to convert rates into an equivalent if Medicare methods had been used. Methods to convert negotiated rates into Medicare equivalents might have varied among the participating insurers, but this is unlikely to affect patterns of variation in rates across markets and within markets. Generally, insurers reported payment rates for large numbers of hospitals in each market. For example, one insurer reported the number of contracted hospitals ranged from 18 in Richmond to 85 in Los Angeles. Insurers were asked to limit their responses to rates negotiated for their own networks and not to report rates from any so-called rental networks they use.

Data on both average payment rates for the entire market and distributions of rates within a market were obtained. For physicians, insurers provided data for selected specialties, including primary care, medical specialists, surgical specialists and hospital-based specialists. For both hospitals and physicians, the instructions for reporting the “highest rate” included reporting only those contracts with substantial claims volume. To protect sensitive information, a commitment was made not to publish any payment rate information based on data from less than three insurers. To increase the understanding of and gain richer insights into the quantitative data, interviews were conducted with insurer network contracting executives as well as individuals from professional and trade associations of providers to reflect provider perspectives on these issues at the national level.

The insurers are not representative of all private insurers, with the most apparent difference related to Blue Cross Blue Shield plans in certain markets (in many areas, Anthem’s market share is much larger than the 25 percent weighting it gets for seven areas in this analysis and the zero weight it gets for Miami, where it does not operate). But with the focus of the study on variation in prices across markets and across providers within a market, the limitation of this convenience sample is likely to be small. The study is vulnerable to instances in which the insurers used different methods to get the specific information requested from their data bases. Although this does not contribute bias, it does detract from the precision of the specific numbers reported. Table 3 (physician payment) could not include the highest rates because of inadequate rates of information submission. A very small number of insurer reports of rates at the 75th percentile appeared to be outliers (all high values). Rather than eliminate these suspected outliers, they were weighted at 50 percent.

Funding Acknowledgement:

This research was commissioned by Catalyst for Payment Reform (CPR). On behalf of large employers, the independent, nonprofit CPR works to drive improvements to how we pay for health care to signal strong expectations for better and more cost-effective care. Working closely with payers, consumers, and providers, CPR aims to identify and coordinate workable reforms, track the nation’s progress, and promote alignment between the public and private sectors. For more information, visit www.catalyzepaymentreform.org.

Back to Top

RESEARCH BRIEFS are published by the Center for Studying Health System

Change.

600 Maryland Avenue, SW, Suite 550

Washington, DC 20024-2512

Tel: (202) 484-5261

Fax: (202) 484-9258

www.hschange.org