Issue Brief No. 119

March 2008

Ann Tynan, Jon B. Christianson

Health plans have expanded consumer-directed health plan (CDHP) product offerings—typically high-deductible health plans coupled with a spending account—and more employers are offering these products to workers, according to findings from the Center for Studying Health System Change’s (HSC) 2007 site visits to 12 nationally representative metropolitan communities. In developing CDHPs, health plans are responding to a broader employer strategy to confer more responsibility on workers for their health care costs, lifestyle choices and treatment decisions. CDHP adoption by employers and consumers depends on a range of factors, including product features and employer characteristics, and varies across the 12 communities. While more large employers are introducing CDHPs into health benefit programs, adoption of CDHPs remains modest. Health plans and employers expect CDHP enrollment to grow as employers and employees become more knowledgeable about CDHP features, health plans develop more sophisticated support tools for plan enrollees, and there are more opportunities to learn from early adopters’ experiences.

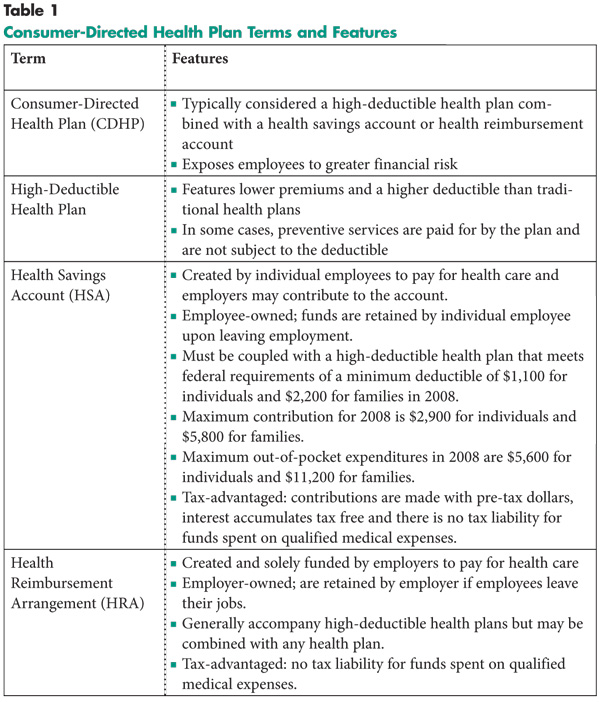

![]() onsumer-directed health plans—typically a high-deductible

health plan accompanied by either a health reimbursement arrangement (HRA) or

health savings account (HSA)—are relatively new additions to health plans’

product portfolios and employers’ health benefit offerings (see Table

1). HRAs, established through U.S. Treasury guidance in 2002, are spending

arrangements owned and solely funded by employers. HSAs were created through

federal legislation in 2003 and are employee-owned and portable—employees retain

balances if they switch health plans or leave their jobs. Both employees and

employers can contribute to HSAs, but contributions are optional. National surveys

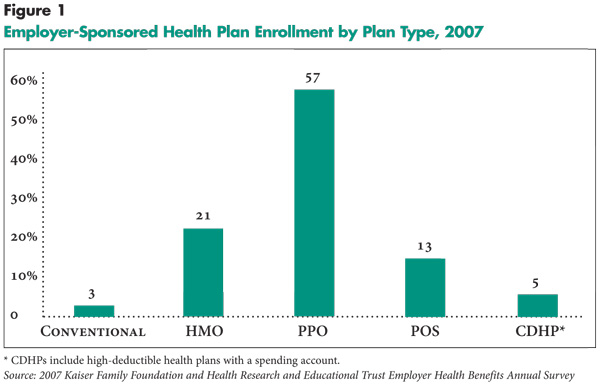

suggest that while CDHPs are being offered by a growing number of employers,

enrollment in these products constituted just 5 percent of total enrollment

in employer-sponsored health plans in 2007 (see Figure 1).

onsumer-directed health plans—typically a high-deductible

health plan accompanied by either a health reimbursement arrangement (HRA) or

health savings account (HSA)—are relatively new additions to health plans’

product portfolios and employers’ health benefit offerings (see Table

1). HRAs, established through U.S. Treasury guidance in 2002, are spending

arrangements owned and solely funded by employers. HSAs were created through

federal legislation in 2003 and are employee-owned and portable—employees retain

balances if they switch health plans or leave their jobs. Both employees and

employers can contribute to HSAs, but contributions are optional. National surveys

suggest that while CDHPs are being offered by a growing number of employers,

enrollment in these products constituted just 5 percent of total enrollment

in employer-sponsored health plans in 2007 (see Figure 1).

HSC researchers reported two years ago that employers were being cautious about introducing CDHPs to their employees.1 In the last two years, the pace of introduction of CDHPs into the health benefit programs of large employers has increased, according to findings from HSC’s 2007 site visits (see Data Source). And health plans and benefits consultants predict more employers will offer these products in the future as momentum strengthens for greater consumer engagement in health care. An economic downturn might also prompt more employers to move in this direction. However, other respondents observed that relatively low premium increases in the last two years have reduced the pressure on some employers to introduce CDHPs, reasoning that more modest premium increases can be addressed by employers through increased patient cost sharing in traditional health maintenance organization (HMO) and preferred provider organization (PPO) products.

|

|

![]() n marketing to large employers, plans position CDHPs as part of a larger consumer-based strategy, where consumers take more responsibility not only for costs, but also for lifestyle choices and treatment decisions. A Cleveland plan respondent observed, “HSAs are just one piece, and employers are looking for an overall strategy.” Other key components of the strategy often include disease management and health promotion and wellness programs.

n marketing to large employers, plans position CDHPs as part of a larger consumer-based strategy, where consumers take more responsibility not only for costs, but also for lifestyle choices and treatment decisions. A Cleveland plan respondent observed, “HSAs are just one piece, and employers are looking for an overall strategy.” Other key components of the strategy often include disease management and health promotion and wellness programs.

In the last two years, many health plans also have developed various consumer-support tools, such as online information about hospital and physician quality and efficiency; tools to help enrollees estimate the costs of care; and information about healthy lifestyles and treatment decisions. When health plans offer consumer-support tools, they generally make them available to all enrollees, irrespective of benefit design. Plans believe that having CDHP benefit designs and consumer support tools are essential to “get in the door” when marketing to employers of all sizes. Increasingly, employers prefer to use a single carrier for all of their health plan offerings, which plans say requires them to offer a full range of products, including CDHPs, to remain competitive.

As part of their consumerism strategy, some employers contribute more to spending accounts if employees attend health behavior modification programs or complete health risk assessments. These assessments, often available online, are used to collect information about such topics as personal and family medical history, current diagnoses or symptoms, and health behaviors related to diet, physical activity, and tobacco and alcohol use. For instance, in a CDHP product offered by a health plan in Indianapolis, funds—from $50 to $250—are automatically deposited in enrollees’ HSAs as a reward for participation in health prevention or improvement activities.

![]() doption of CDHPs by employers and employees is influenced by many factors, including product features and employer characteristics, such as the workforce size and type. The importance of these factors varied across the 12 communities.

doption of CDHPs by employers and employees is influenced by many factors, including product features and employer characteristics, such as the workforce size and type. The importance of these factors varied across the 12 communities.

Complexity of Products. The complexity of CDHP product designs is a concern for some employers. They believe that CDHPs are difficult for some employees to understand and, therefore, require extensive employee education when offered. Some large employers reported spending 12 to 18 months educating employees before rolling out CDHPs. Employees must understand the federal tax rules and regulations governing HSAs, including contribution caps and what medical expenses can be paid using HSA funds. Further, consumers may have to shop for an HSA provider to administer the account if their employer does not contract with one.

Some employers perceive the portability of HSAs as a negative feature, especially in industries with high employee turnover. These employers respond by not contributing to the account (or contributing little) or by offering an HRA instead. A few employers reported substantial end-of-the-year use of care by employees who had exceeded the plan deductible—a possible response under all high-deductible benefit designs. Employee ability to shift care from years in which the deductible may not be met to years when it is met diminishes the potential savings from these benefit designs, in the view of some respondents.

Employer Characteristics. The factors that affect CDHP adoption vary for large vs. small employers. Large employers sometimes value CDHPs as part of an overall strategy to shift more responsibility for health care to employees but are hesitant to structure benefit designs and premiums to incorporate strong incentives to steer employees to these plans. For the most part, benefits have been structured to date to make the required employee contribution similar across health benefit options. These large employers are emerging from a period of substantial increased patient cost sharing through higher deductibles, coinsurance and copayments. For fear of a negative employee response, they are reluctant to shift completely to a new plan design that employees may perceive as less comprehensive with additional cost sharing.

Recognizing the hesitancy of some employers to offer HRAs or HSAs, health plans are helping employers to transition toward these products. For example, a Cleveland health plan offers a PPO option accompanied by health coaching, other consumer-support tools and monetary incentives offered to employees for participating in activities to maintain or improve their health. Larger employers with young, highly educated workforces are not as concerned that the perception of less comprehensive benefits in a CDHP will hinder recruitment and are more confident that workers will be able to use the online consumer information support tools to make informed choices.

Smaller employers with low-wage workforces typically offer an HSA as an embellishment to a high-deductible plan and often do not contribute to the account. According to respondents, most small employers cannot afford to pay for their employees’ health care premium increases. For some small employers, the lower cost of CDHPs makes them the last option before discontinuing health benefits altogether. Observers attribute the popularity of CDHPs, particularly with HSAs, with small employers in Greenville to the fact that many consumers in this market already are accustomed to plan designs with relatively large deductibles and coinsurance requirements—features small employers previously introduced to limit premium increases.

In contrast, smaller employers with high-wage professionals are more likely to offer HSAs because employees value the tax advantages. These employers also are more likely to contribute to employees’ accounts. Small employers, regardless of type, are more likely to offer HSAs as a “total-replacement” product, with coverage and plan design features varying depending on whether the workers are high or low wage. In some communities—Orange County in particular—some smaller employers are working with third-party administrators (TPAs) to “build their own” HRA-type plans. Under this approach, an employer purchases a high-deductible health plan and then separately sets up an HRA account, using a TPA and a broker to administer it.

Employers with high workforce turnover, such as the retail industry, are more likely to offer and fund HRAs than HSAs. According to one respondent, “HRAs are good for employers with a lot of turnover since the money stays with the employer in an HRA.” For example, in January 2007, two large retailers in Indianapolis and Phoenix began offering HRAs to their employees. A large local supermarket chain in Indianapolis replaced its PPO options with a high-deductible plan and HRA. The large Phoenix retailer offered employees a choice of several PPO products accompanied by HRAs. According to the employer, “We chose the HRA over the HSA due to our industry and turnover. We were reluctant to fund an HSA since we have an 80 percent turnover rate.”

Public employers generally have not added CDHPs with HSAs or HRAs to benefit offerings because their employees are accustomed to comprehensive benefits, often negotiated through union contracts. Instead, public employers continue to rely on incremental cost shifting in the form of higher deductibles, coinsurance and copayments in existing products. Some reportedly intend to introduce HSAs and HRAs in the future, after employees have had more experience with higher deductibles.

State governments in Indianapolis and Little Rock do offer CDHPs to employees and continue to refine their offerings to encourage enrollment. In 2006, the state of Indiana introduced a high-deductible plan with an HSA for state employees, but only 4 percent of employees enrolled. In 2007, it added a second HSA plan with a lower deductible. Enrollment in 2007 increased to about 16 percent, which one respondent primarily attributed to the state’s decision to include full coverage of preventive services, such as annual well-care visits, mammograms, prostate screenings and immunizations, in its CDHP offerings.

Similarly, the state of Arkansas has offered a high-deductible plan with an HSA for the past four years and has lowered the deductible from $1,500 single/ $3,000 family to $1,250 single/ $2,500 family to make the plan more attractive. Enrollment reportedly continues to grow, especially among employees under 35 years old, who perceive themselves as healthy and expect few expenses, and employees over 55 years old, who value the HSA as a retirement investment vehicle. Despite the relative success of the HSA product for that employer, another public employer in Arkansas believes employees would be resistant, saying, “I would be crucified if I offered an HSA.”

Employers operating in highly competitive labor markets tend to offer more comprehensive health benefits and seem more cautious in their approach to CDHPs. According to a Little Rock health plan respondent, “Employers continue to use health care benefits to attract good employees, so if they go with CDHPs it might be viewed negatively because CDHPs cause employees to face more out-of-pocket costs.” In Orange County and Boston, where HMO enrollment continues to be strong, many respondents view HMOs as offering more coverage at a lower price than plans with HSAs and HRAs. This makes it difficult for CDHPs to compete, as long as employees and employers are willing to accept some restrictions in provider networks. In other communities—such as Cleveland, Lansing and northern New Jersey—unions are strong, and they typically see CDHPs as offering less comprehensive benefits. Therefore, they resist employer attempts to introduce these plan designs into health benefit offerings.

![]() lan respondents and benefit consultants generally expect CDHPs to play a more prominent role in employer health benefit offerings in the future, especially as part of broader strategies to increase employee responsibility for, and involvement in, managing their health care. For now, many large employers are engaged in “watchful waiting.” They are offering CDHPs as options, hoping that employees will become more comfortable with the product designs over time, so that eventually other options can be dropped or restructured to favor the choice of an HSA/HRA. They also are hoping to learn from the experiences of the few large employers that have replaced all benefit options with CDHPs.

lan respondents and benefit consultants generally expect CDHPs to play a more prominent role in employer health benefit offerings in the future, especially as part of broader strategies to increase employee responsibility for, and involvement in, managing their health care. For now, many large employers are engaged in “watchful waiting.” They are offering CDHPs as options, hoping that employees will become more comfortable with the product designs over time, so that eventually other options can be dropped or restructured to favor the choice of an HSA/HRA. They also are hoping to learn from the experiences of the few large employers that have replaced all benefit options with CDHPs.

Some large health plans, such as Aetna and UnitedHealthcare, and national benefit consultants, Towers Perrin and Watson Wyatt, are setting an example for their clients by replacing benefit options with CDHPs for their own employees. All respondents agreed a carefully planned and executed approach to implementation was needed to educate employees regarding product features and to alter existing benefit coverage so that HSAs and HRAs could be priced competitively.

There was less consensus among respondents regarding the future of CDHPs for small employers. Respondents expected HSAs to continue to be adopted in high-income professional firms because of substantial tax advantages. For lower-wage, small firms, respondents believed the larger issue was whether or not these employers would continue to offer health insurance at all. HSAs might be offered by some with high-deductible plans, but without employer contributions to savings accounts.

Several respondents referred to the 2006 changes in HSA laws as having the potential to stimulate enrollment growth, particularly among higher-wage workers. Federal legislation passed in December 2006 increased the maximum amount that employees and employers can deposit to health savings accounts.2 As one respondent characterized it, “HSAs are a potential vehicle for wealth accumulation; they are designed to amass more money for health benefits and are better than a 401(k) plan.” One respondent reported observing a shift in employers’ focus from HRAs to HSAs in light of the new legislation. Although the legislation’s timing was such that it did not have an impact on the 2007 benefit year, respondents expected the impact to be more evident in 2008.

![]() n the past two years, health plans have expanded CDHP offerings in response to employer demands for products that support broader consumer-based strategies, where workers take more responsibility for health care costs, lifestyle choices and treatment decisions. However, large employers generally have not yet structured their premium contributions to favor these options.

n the past two years, health plans have expanded CDHP offerings in response to employer demands for products that support broader consumer-based strategies, where workers take more responsibility for health care costs, lifestyle choices and treatment decisions. However, large employers generally have not yet structured their premium contributions to favor these options.

With plan choice less practical for small employers, those offering a CDHP tend to make it the sole option. While respondents are optimistic that CDHPs will become more prominent in health benefit offerings, fostering greater employee take-up may require health plans and employers to make HRAs and HSAs more appealing—perhaps by further refining consumer-support tools and increasing employer contributions to spending accounts.

Recent steps by some employers to reward employee participation in health promotion and wellness programs with larger contributions to employee spending accounts may create a new “competitive advantage” for CDHPs if a substantial number of other employers adopt similar strategies.

Every two years, HSC conducts site visits in 12 nationally representative metropolitan communities as part of the Community Tracking Study to interview health care leaders about the local health care market and how it has changed. The communities are Boston; Cleveland; Greenville, S.C.; Indianapolis; Lansing, Mich.; Little Rock, Ark.; Miami; northern New Jersey; Orange County, Calif.; Phoenix; Seattle; and Syracuse, N.Y. Approximately 500 interviews were conducted between February and June 2007 in the 12 communities. In each community, representatives from at least two of the largest health plans were interviewed. Health plan representatives included the medical director, a marketing executive, and a network executive. Interviews also were conducted with benefit consultants, brokers and representatives of at least two large employers.

ISSUE BRIEFS are published by the

Center for Studying Health System Change.

600 Maryland Avenue, SW, Suite 550

Washington, DC 20024-2512

Tel: (202) 484-5261

Fax: (202) 484-9258

www.hschange.org